Last week, I wrote about the amazing welcome bonus offers on the Personal (100k-125k) and Business (95k) versions of the Amex Platinum Card. The public offer for the personal Platinum Card is for 100,000 Membership Rewards points + 10x points on grocery and gas purchases. Some folks are also seeing an elevated offer for 125,000 Membership Rewards points. Many people are wondering how they can maximize the category bonuses and max out the 10x spend up to $15,000 in the first year. If you don’t have organic spend, you may be tempted to buy gift cards. However, American Express is known to be particularly vigilant about cracking down on what they define as suspicious of ‘gaming’ related behavior. The last thing you’d want after getting an amazing offer is to get shut down by American Express. How do you maximize these bonus offers without raising any alarms? Let’s have a look.

Creating a Framework

There’s no dearth of information about reports of customers getting shut down by American Express. However, I was hoping to come up with a framework that would help readers figure out what’s happening. Should all of us be worried? If not, what should be the level of concern? What does Amex consider as shady behavior?

At a very basic level, I tried to break these down into two different buckets. One is the type of action you take. The second bucket is Amex’s reaction to it. Quite often the level of panic is dictated by the severity of action that Amex takes. Does American Express simply claw back points or shut down your account altogether?

Levels of Escalation

If you look at some of the discussions happening on Reddit and Flyertalk, there are certain types of actions that evoke a reaction by Amex. If Amex doesn’t like what you’re doing, they’ll probably do one of three things:

Denials: They will deny you when you apply for a card or simply deny you the welcome bonus after you’re approved for the card, if they suspect that you’re gaming the system. You’ll probably just see the dreaded pop-up when you apply.

Clawbacks: This means that Amex is taking much more than a cursory glance at what you’re doing. For example, a few years back, Amex temporarily froze accounts of customers who had applied for the 100k Amex Platinum offer that wasn’t quite meant for them. Most recently, we’ve seen Amex claw back points from customers who’ve done a lot of self-referrals. On Reddit, some people have reported that Amex has in some cases clawed back up to 100,000 Membership Rewards points for self referring.

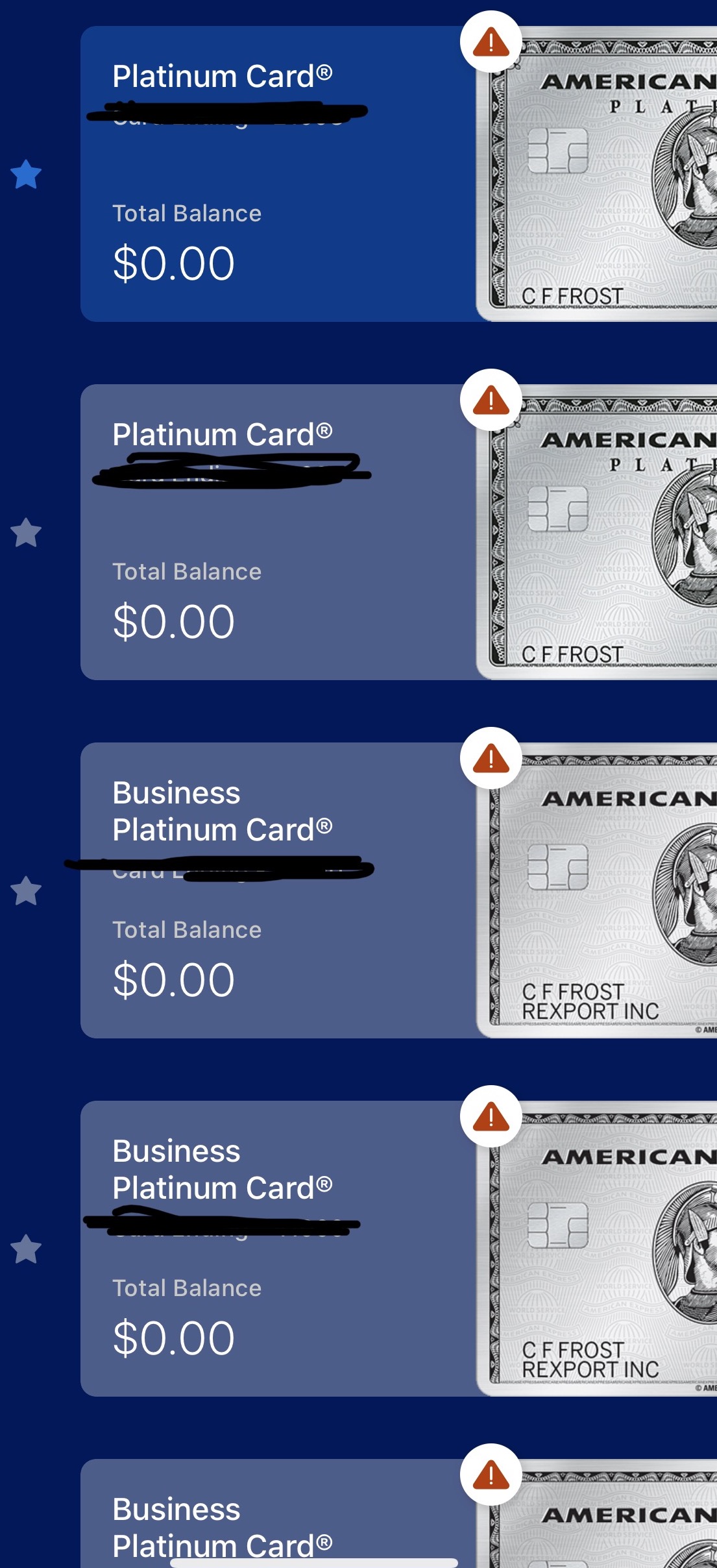

Shutdowns: This is the red line. It means that Amex has had enough and that they don’t think you’re worthy of keeping as a customer. A reddit user posted a screenshot of how your Amex account looks once the dreaded message appears on your screen. What’s striking is that this person has multiple types of the same card – 2 Personal Platinum Cards and 3 Business Platinum Cards.

A reddit user shared his plight after being shut down

Bad Behavior

So which are the bad actions that may prompt Amex to take a second look at your account? If you want to prevent any undue attention, it may be prudent to stay away from doing any of these things. Again, it’s not necessary the simply one of these actions would lead to a shut down. However, a combination of one of more of these actions would definitely invite a scrutiny of the account.

- Heavy Manufactured Spending

- Applying for a sign-up bonus that wasn’t meant for you (Most recent shutdowns due to applying for no lifetime language offers)

- Multiple Self-referrals

- Selling points

- Multiple pay over times

- Credit Cycling

- Late Payments

- Exceeding Credit Limits

- Constant Churning

- Closing or downgrading your card in less than 12 months after receiving the welcome bonus

Analysis

I think there are a few aspects that need to be looked at. Magnitude is vital when it comes to the measurement of these actions and what the ensuing ramifications may be. Ask yourself these questions. These may give you a better representation of where you stand when it comes to attracting Amex’s fraud prevention teams.

- What’s your ratio of organic spend to manufactured spend?

- Do you have a steady predictable spending pattern?

- What’s your length of association with American Express? Is your first American Express card still open?

- Have you held an Amex card for many years on which you’ve been paying the annual fee year after year?

- Is your spend exponentially high at any single merchant? (For example, Gift card mall)

- Are you constantly churning Amex cards? (Signing up, getting the bonus and then canceling)

- If asked, can you provide substantial documentary evidence to prove your income and other assets?

The Pundit’s Mantra

I’ve written previously about avoiding the crash and burn approach and why it’s bad. Miles and points aren’t going anywhere. The risks you take to earn those extra miles are never worth risking a shut down by a major card issuer. From the data above it seems like if you’ve done multiple self-referrals, hold multiple of the same credit cards and do heavy manufactured spending in bonus categories, you may well be on Amex’s radar already.

On one hand, I’m glad to see many issuers offering really high welcome bonuses, well upwards of 100,000 points. On the other hand, one must also be careful while maximizing these offers. Card issuers can exercise very broad discretion and it always helps to stay in the good books of major card issuers.

___________________________________________________________________________________________________________________

Never miss out on the best miles/points deals. Like us on Facebook, follow us on Instagram and Twitter to keep getting the latest content!

___________________________________________________________________________________________________________________

Disclosure: The Points Pundit receives NO compensation from credit card affiliate partnerships. Support the blog by applying for a card through my personal referral links. This article is meant for information purposes only and doesn’t constitute personal finance, health or investment advice. Please consult a licensed professional for advice pertaining to your situation.