‘Limited time offer’ is probably the most eye catching headline for miles and points lovers. It attracts attention, starts a dialog and often leads to heated discussions. However, are these limited time credit card offers really good deals or simply marketing gimmicks?

If you refer to my very first post on this blog, you’ll see that I often talk about using your own discretion while signing up for some of the best miles and points credit card offers. A lot depends on your location, airline availability at your local airport and your choice of hotel benefits.

Credit Card Offers can be tempting, but choose wisely (Image Credit: Unsplash)

So why do limited time offers on credit cards garner so much attention? Are they all just hype? Let’s have a look.

Buyer Behavior

Credit card companies have marketing departments which focus solely on customer acquisitions. Their incentives are determined by a combination of factors, with one of the primary ones being new customer sign ups. They are incentivized to have as many people sign up for the card as possible.

Credit card companies know that buyer behavior is often irrational. Credit card bonuses need to be looked at as rebate programs. When you spend x amount of dollars, you get certain benefits to which you can ascribe a dollar value.

Brands are fighting to capture our attention

Limited Time Offers

We usually see two types of limited time offers. One of them is with a specific end date, while another one is open ended. The open ended ones are trickier because they often don’t have an end date and can be pulled at any time. However, they also help create an artificial scarcity in the minds of the consumer. You often wonder – Will this offer still be around later? and end up signing up for the card.

Creating the Urgency

A lot of times we see offers disappear after an end date, only to return after a while. This could probably because the team didn’t meet its sales target and wants to reintroduce the offer to attract more credit card sign ups.

Travel Goals

The only factor that should decide if you should sign up for a credit card is your travel goals. I’m passing the recent 100,000 mile Capital One offer because it doesn’t align with my travel goals. I have hefty points balances in my Amex and Chase accounts, and continue to use their transferable partners to book my travel. Also, Capital One pulls all bureaus and can be a really tough issuer to get approved for.

Signing up for a limited time offer is of no use if you are just going to let those miles sit in your account merely for the process of accumulation. Miles and points in general lose value over time, so it makes no sense just to accumulate them without having any particular idea about redeeming them.

Referral Offers

A lot of times you’ll see better offers if you use your own referral links to refer a friend. I’ve found this to be true about a lot of American Express offers that I’ve seen through personal referral links.

You can refer friends for certain credit cards

Shopping Cart Trick

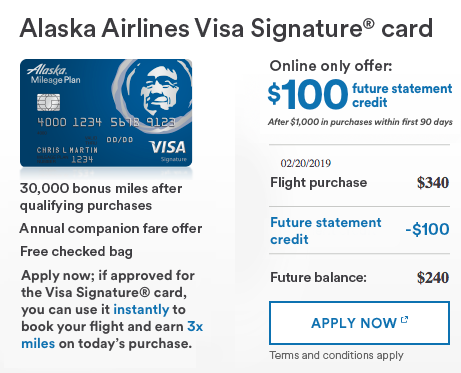

Ultimately it’s all about running the numbers. Marketers run A/B tests all the time. The idea is to run two or more variants of the same offer in order to better understand buyer behavior. I keep getting offers in the mail for the Bank of America Alaska Airlines card for a sign up offer of 40,000 Miles after spending $2,000 in 3 months. The card has a $75 annual fee.

However, I went to the Alaska Airlines website and started making a dummy booking. After entering all the details, here’s the offer that came up. In fact, there’s also a current public offer of 65,000 miles after $8,000 in spend.

40k Miles with $75 AF or 30k miles + $100?

So which offer is better? Would you rather save on the annual fee with the statement credit or earn the extra 10,000 miles? If your goal is to fly in business class, then those extra 10,000 miles might be worth for you for a small price of $75. If your goal is to fly as much as possible for the least amount spent out of pocket, then the offer in the picture above might just suit you best.

Similarly, if you go for the 65,000 mile offer, you’ll have to spend an additional $6,000 to pocket the extra 25,000 miles.

The Pundit’s Mantra

Credit card companies are businesses that run in order to make a profit. They’re looking to attain sales quotas, acquire customers and meet targets. In the same way, before you sign up for a credit card, have a look at your personal finances and travel strategy. Given a combination of those two factors, which card would be the most suitable for you? Which offer have you jumped on recently? Tell us in the comments section.

___________________________________________________________________________________________________________________

The Points Pundit loves these newly relaunched Chase credit cards!

Firstly, they offer you a 0% APR for the first 15 months.

Secondly, they have no annual fee and have a lucrative welcome bonus of $200 or 20,000 Ultimate Rewards points after you spend $500 in the first 3 months.

They’re packed with brand new benefits and bonus points categories.

Overall, a great option to carry in your wallet for everyday spend!

(Chase’s 5/24 rule may apply to these cards)

___________________________________________________________________________________________________________________

Never miss out on the deals, analysis, news and travel industry trends. Like us on Facebook, follow us on Instagram and Twitter and get the latest content!

___________________________________________________________________________________________________________________

Disclosure: The Points Pundit receives NO compensation from credit card affiliate partnerships. Support the blog by applying for a card through my personal referral links. This article is meant for information purposes only and doesn’t constitute personal finance, health or investment advice. Please consult a licensed professional for advice pertaining to your situation.