Chase 5/24 became the talk of the town every since Chase introduced it as an unwritten rule. In this post, I also argued as to how it was very smart marketing strategy. The Chase 5/24 rule was aimed at discouraging churners. In short, churning is an activity where you get a credit card just for the welcome bonus, cancel it after the first year and move to the next one. Chase 5/24’s intent was to make consumers prioritize Chase cards over their competitors. Also, it meant that Chase had clearly defined the kind of customers they desired. However, as the markets tank and enter a recession, do these guardrails really even matter?

Chase 5/24 Status

As per Chase 5/24, Chase will not approve you for their cards if you’ve been approved for more than 4 cards from any bank in the last 24 months. In short, Chase determines that anyone who gets more than 4 cards in a 24 month period is likely to churn and isn’t worth acquiring as a customer.

Market conditions have changed drastically in the last quarter. Here’s why Chase 5/24 won’t really matter in the short run.

Decrease in Credit Card Applications

As per this CNBC report, we’re seeing a 40% drop in credit card applications already. This shows that consumers aren’t simply applying for credit cards at the same rate as they were before the recession hit.

Decrease in Credit Card Spend

Financial Times reports about the drastic fall in spend on credit cards. This also shows that not only are consumers not getting new cards, they aren’t spending the same on existing ones. In short, people aren’t using their credit cards at the same rate.

Credit Card Approvals

Even if you intend to churn, banks simply aren’t approving people at the same rate. We’ve already seen multiple reports where major issuers like Amex and Chase are issuing denials to customers.

Also, Doctor of Credit recently reported data points that Amex may also be tightening the screws with a new ‘4 card limit’. If banks simply stop approving customers at the same rate, your 5/24 status will not really be impacted.

Q2 Data and Q3 Forecast

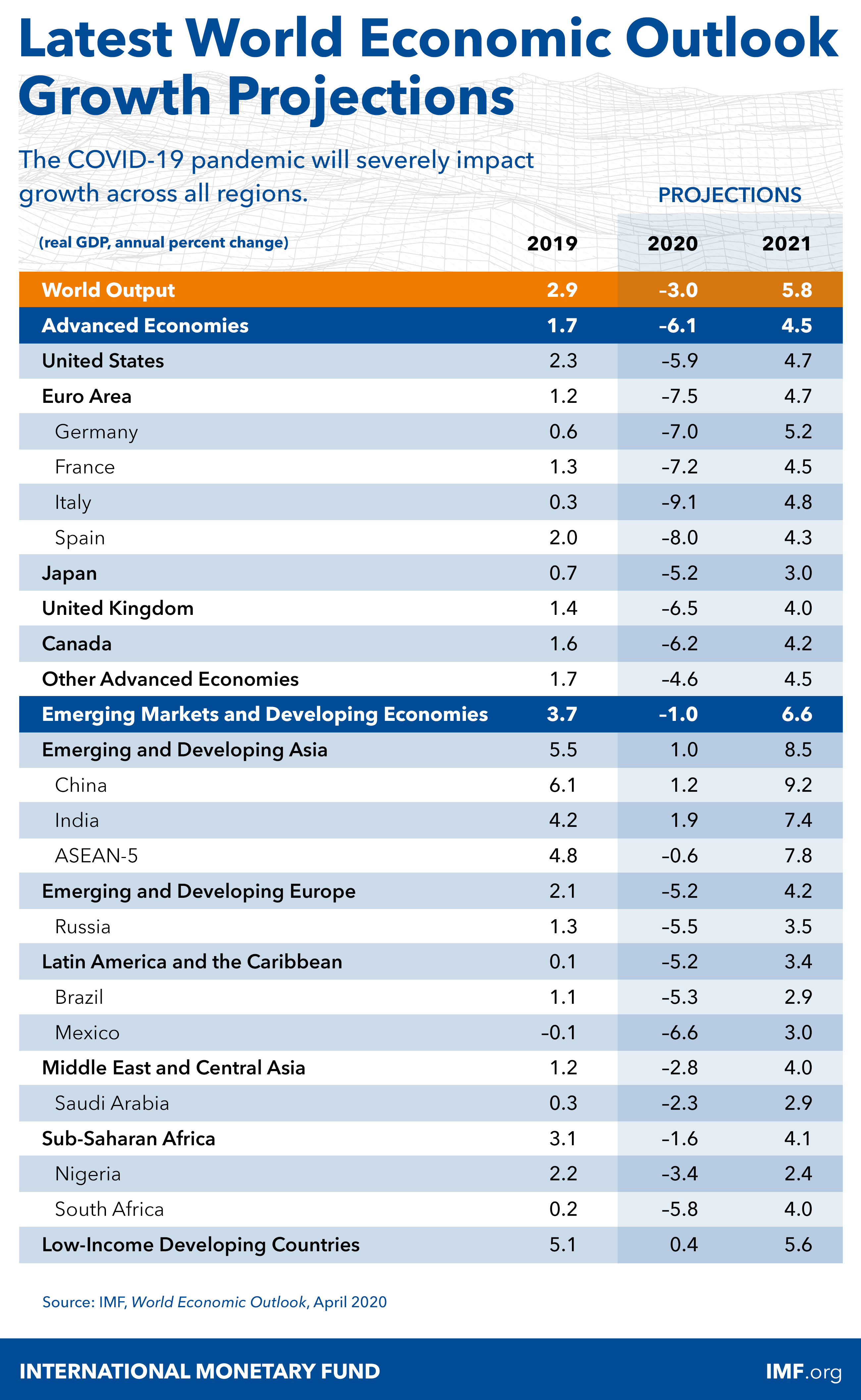

Recently, JP Morgan Chase CEO Jamie Dimon opined that we’re in a bad recession. During their most recent earnings call, Chase execs also mentioned that they don’t really have enough data yet to make a determination about how badly consumers are hit. In simple terms, much of Q2 will show the first signs of the real impact of Covid-19 on the economy. However, bank execs themselves say that they’ll remain cautious as they wait for the full Q2 data to come in before they make any predictions about a possible recovery.

Unemployment, it looks like 30%, 40% of people going on unemployment book higher income than before they went on unemployment. So what does that mean for credit cards and something like that? Or that the government is just going to make direct payments to people. So this is all in the works right now. – JP Morgan Chase CEO Jamie Dimon

Boeing’s CEO recently said in an interview that he expects that one major US airline may not survive the recession by the end of the year. He also expects airline demand to recover to just 50% by holiday season. Given the weak customer demand, many people will be sitting on a lot more miles and points than they can use. In such a case, adding more miles and points with no immediate use could do more harm than good, as evidenced by the most recent devaluation.

Chase Credit Cards

Also, are Chase cards as desirable as they were a few years ago? We haven’t seen Chase offer a 100k welcome bonus since they first launched the Sapphire Reserve. United has now devalued their miles by removing award charts. In my opinion, that has definitely reduced the value of the Chase Ultimate Rewards program. Chase launched the new World of Hyatt credit card with a 60k welcome bonus. However, we’ve only seen the 50k bonus ever since.

Chase isn’t offering very attractive bonuses on many of their cards. In such a case, many would simply wait to fall under 5/24 to get the one card they desire. For those above 5/24, they may not be simply missing out on much right now. Also, Chase 5/24 isn’t the only restriction though. We also have the One Sapphire Rule and the 2/48 rule to worry about.

In addition, many data points suggest that Chase is making business card approvals tougher. According to this article by Miles to Memories, Chase may require you to have a business checking account before they approve you for a new business credit card.

In conclusion, Chase’s current welcome bonuses aren’t very attractive and their cards are harder to get in the short run.

Minimum Spend Requirement

When major issuers offered extra time to customers to meet minimum spend, we saw the first signs of where the market was heading. People simply aren’t spending enough and as frequently. In response, banks are now offering customers more time.

In simple terms, if fewer people are meeting minimum spend at a slower rate, people may simply not be applying for credit cards at the same pace. If people are just sitting an waiting it out, then it means that dropping under 5/24 is just a matter of time as they wait for the storm to pass. Also, due to many states imposing lockdowns or closures, many manufactured spending options have also dried up.

The Pundit’s Mantra

The world has changed drastically in the last few weeks. We’re seeing the worst rate of unemployment since the depression. The labor department estimates that over 20 million people lost their jobs in April. Why does this matter? It means people will simply have less or no disposable income in the short run.

With rising debt and joblessness, people will focus a majority of their spend on necessities instead of luxuries. Travel is one of those luxuries. With the travel industry in the doldrums, it’s no surprise that we’re seeing a drastic fall in consumer spending in the dining and travel category.

I haven’t applied for any new credit cards this year. While I had a few on my radar, I’ve decided to wait it out after the recession hit. Like many frequent travelers, I’m sitting on a heap of miles and points. Once the storm passes and the economy rebounds, we’ll likely see reduced restrictions and better welcome offers from most issuers. I plan to jump on to those lucrative offers when travel is fully operational and when I can see myself using those miles or points for an upcoming trip.

Are you still thinking about the Chase 5/24 rule or simply focusing on other cards? If yes, which Chase card do you intend to get the next time you apply? Tell us in the comments section.

___________________________________________________________________________________________________________________

Disclosure: I receive NO compensation from credit card affiliate partnerships. Support the blog by applying for a card through my personal referral links

___________________________________________________________________________________________________________________

Never miss out on the best miles/points deals. Like us on Facebook, follow us on Instagram and Twitter to keep getting the latest content!

I mean, it will still serve to stop churners right? I guess you are arguing that people won’t churn during the pandemic? Not sure about that.

This sentence is wrong btw – “As per Chase 5/24, Chase will not approve you for their cards if you’ve been approved for 4 or more cards from any bank in the last 24 months“

Hi Bob,

Thanks for pointing that out. Just updated it.

Well, the nub of the argument is that market conditions and risk aversion will automatically shrink the number of opportunities for customers to obtain new credit. The Chase 5/24 rule was instituted when market conditions were much different and when Chase was simply looking to cut costs on welcome bonuses by dissuading churners. In this hobby, dropping under 5/24 was a big deal as it gave you access to Chase’s products and lucrative bonuses.

In addition, it will be a while before airlines and hotels will be fully operational for us to use the miles and points we’ve earned. In such a scenario, your 5/24 status won’t matter much. In a nutshell, market conditions, lower bonuses and a lack of immediate travel opportunities will automatically result in fewer people applying for credit cards, thereby rendering Chase 5/24 obsolete as a barrier in the short run.